Turning Points: Your Decade-by-Decade Guide to Retirement Milestones

By Myla Pacis

Regional Vice President, FEG

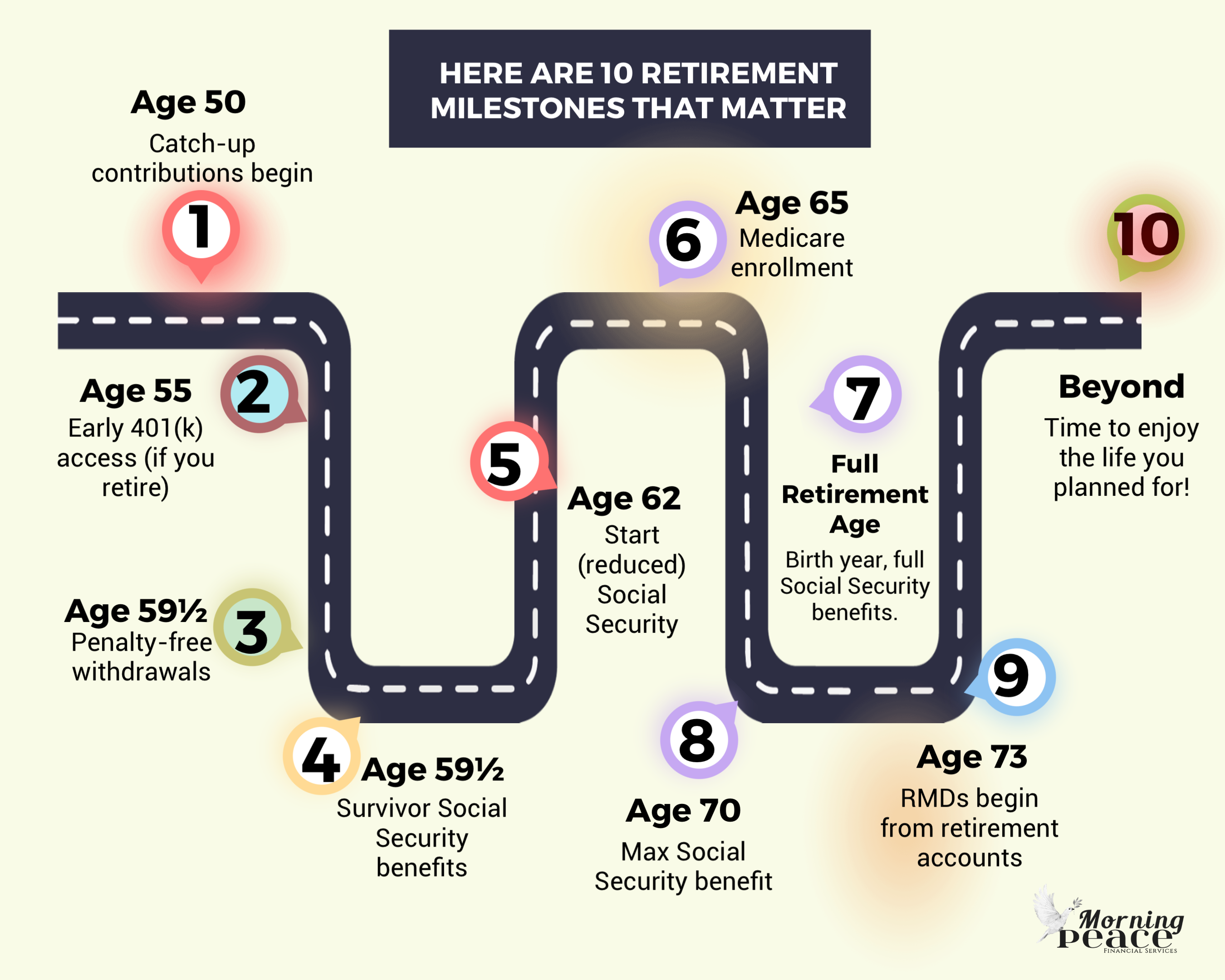

You've hit 50 – big congrats! This milestone isn't just symbolic; it opens new doors for retirement planning. You're now eligible for catch-up contributions, as defined by the IRS. This allows you to contribute more to your traditional 401(k) and IRA accounts, helping you make up for earlier years where saving might have fallen short.¹

Planning to Retire Early?

If early retirement is on your radar, the Rule of 55 is worth understanding. It allows penalty-free withdrawals from an employer-sponsored 401(k) if you leave your job the year you turn 55 or later – assuming your plan permits it.² This rule can be a helpful strategy if you're planning to step away from work ahead of the typical retirement timeline.

Approaching 60? More Options Open Up

As you near your 60s, access to your retirement savings changes. At age 59½, you can begin withdrawing from traditional IRAs and most retirement plans without facing the 10% early withdrawal penalty.³ While income taxes may still apply, you now have more flexibility in how and when you use your savings.

Time to Take Stock

With early withdrawal penalties mostly behind you, it's a great time to pause and evaluate your retirement picture. Have your financial needs changed? Are you still planning to retire early, or do you need to pivot? Even without penalties, there are still tax implications tied to withdrawals. A financial advisor can help ensure you're staying on track and optimizing your strategy.

Social Security: It Begins

At 60, Social Security Survivor benefits become available. If your spouse – or even a former spouse of at least 10 years – has passed away, you may be eligible to claim benefits.⁴

Social Security: It's Officially on the Table

At 62, you can begin drawing Social Security benefits, but keep in mind: starting early usually means a reduced monthly benefit. If you're still working, your benefits might be further reduced until you reach full retirement age. For full details, visit ssa.gov.

Welcome to Medicare

Healthcare plays a crucial role in retirement. If you're no longer on an employer-sponsored health plan, Medicare eligibility begins at age 65. You can enroll as early as three months before your 65th birthday. Already receiving Social Security? You'll be enrolled automatically. Visit medicare.gov for all the enrollment details.

Full Retirement Age – You're Here!

Your full retirement age depends on your birth year. Reaching it allows you to collect your full Social Security benefit amount. Not sure when that is? Use this chart from the SSA: Retirement Age Calculator

Age 70: Maximum Social Security Benefits

If you've delayed collecting Social Security, age 70 is the final stop. Waiting has paid off — your monthly benefit has grown about 8% for each year you waited past full retirement age.⁵ There's no benefit to delaying beyond 70, so now's the time to start receiving it.

Required Minimum Distributions (RMDs)

Now it's time to begin Required Minimum Distributions (RMDs) from tax-deferred accounts. The IRS mandates these annual withdrawals to ensure funds are eventually taxed. RMDs count as taxable income, and laws governing them recently changed under the SECURE 2.0 Act. Learn more about these changes and how they affect you at IRS.gov.

You've Reached the Summit

Every retirement journey is unique, and this timeline is just a framework. As you navigate each stage, make sure your retirement income strategy supports your goals and lifestyle. For more tools, insights, and resources to help guide your next steps, click here to learn how American Equity can be a part of your plan.

Footnotes:

- Internal Revenue Service: Retirement Topics - Catch-Up Contributions, August 2023

- IRS: Topic No. 558, Additional Tax on Early Distributions, November 2023

- IRS: Exceptions to Tax on Early Distributions, August 2023

- Social Security Administration: Benefits for Spouses, December 2023

- Social Security Administration: Delayed Retirement, December 2023